Judges Opinions, — October 15, 2015 10:20 — 0 Comments

City of Lebanon, et al., v. Cornwall Borough, et al., v. Lebanon County Earned Income Tax Bureau No. 2012-01222

Civil Law-Law and Equity-Local Government Entities-Erroneous Payment of Tax Monies-Unjust Enrichment-Constructive Trust-Claim under Local Tax Enabling Act-Conversion-Unclean Hands-Prejudgment Interest-Calculation of Interest on Damages-Negligence-Statute of Limitations of Local Tax Enabling Act-Political Subdivision Tort Claims Act-Compensatory Damages-Consequential Damages-Recovery of Litigation Expenses-Recovery of Pre-Litigation Expenses

1. In 2007, the Lebanon County Earned Income Tax Bureau (“the Bureau”) learned that its former executive director, the late Donald Foltz, had embezzled over $800,000.00 in taxpayer money between 2002 and 2006. The Bureau’s bonding agency reimbursed the Bureau for the monies embezzled by Foltz. With the appointment of a new director, it was discovered that distribution of tax monies by the Bureau to municipalities and school districts between the years 2004 and 2007 may not have been proper. As a result, McKonly & Ashbury (“M & A”), an accounting firm selected by the Bureau with the approval of all of its constituent municipalities and school districts, was engaged to recreate an appropriate tax distribution model for the years 2004 to 2007. The performance of that model resulted in the conclusion that eighteen (18) municipalities and school districts had been overpaid tax distributions during those years. Thirteen (13) of the eighteen (18) municipalities identified in the model as overpaid agreed to return the overpayments over an extended period of time. Defendants refused to return the alleged overpayments, asserting that the M & A model was not accurate.

2. Plaintiffs, comprised of the underpaid municipalities as reflected in the M & A model, filed an action against Defendants with claims of unjust enrichment, constructive trust, violation of the Local Tax Enabling Act and conversion, asserting that the monies distributed by the Bureau between 2004 and 2007 were not distributed in a manner matching the intent of the tax ordinances passed by each school district and municipality, resulting in an underpayment of taxes to Plaintiffs and an overpayment of taxes to Defendants. Defendants filed claims against Additional Defendant, the Bureau, in negligence and violation of the Local Tax Enabling Act.

3. A forensic accountant was appointed by the Court as an independent accountant to evaluate the process employed by M & A to determine an appropriate tax distribution model for the years 2004 to 2007, and the forensic accountant stated that to a degree of accounting and professional certainty, the methodology employed by M & A, while admittedly imprecise, was fair and reasonable based upon all facts known to the parties.

4. In determining whether the M & A methodology of calculation to determine overpayments and underpayments was reasonable and credible, the Court found it significant that the Defendants never proffered an alternative distribution proposal regarding the distribution of funds between 2004 to 2007 and instead request that the Court maintain the status quo by essentially endorsing the system of distribution designed by Foltz who had engaged in criminal activity, which the Court found to be unconscionable.

5. The Court held that while imperfect, the methodology utilized by M & A was a fair and reasonable reconstruction of the manner in which the Bureau should have distributed tax revenue between 2004 and 2007 based upon the fact that all of the Lebanon County school districts and municipalities hired M & A to conduct an analysis, a forensic accountant hired by Plaintiffs credibly testified to a reasonable degree of accounting certainty that the M & A methodology was appropriate and generated a proxy result that would be within a reasonable variance as to what the information would have looked like in a perfect world, an independent forensic accountant engaged by the Court indicated that to a reasonable degree of professional certainty that the methodology employed by M & A was fair and reasonable based upon all of the facts known to the parties, the M & A team testified that they expended roughly 500 hours undertaking the analysis and Keystone Tax Bureau’s calculation of accurate distributions between the years 2009 and 2012 so closely aligned with the distribution proposed by M & A and bears little comparison to the actual distributions actually undertaken by the Bureau between 2004 and 2007.

6. Under Pennsylvania law, a plaintiff must prove damages with a fair degree of probability. While damages cannot be based upon mere guess or speculation, where the amount may be estimated fairly from the evidence, recovery will be sustained even though such amount cannot be determined with entire accuracy.

7. The Court concluded that longstanding Pennsylvania precedent requires that when funds mistakenly are paid, the recipient has a moral and an ethical duty to return the funds to their rightful owner.

8. Prejudgment interest may be awarded when the defendant holds money or property that belongs in good conscience to the plaintiff. The determination of whether to award prejudgment interest and the rate of such interest is vested in the discretion of the Court.

9. The elements of unjust enrichment are a benefit conferred upon a defendant by a plaintiff, acceptance of the benefit by the defendant and retention of the benefit by the defendant under circumstances that would render it inequitable for the defendant to retain the benefit. Privity of contract is not necessary to establish a claim for unjust enrichment. The Court found in favor of the Plaintiffs and against the Defendants on the claim of unjust enrichment and directed that the respective Defendants reimburse the Plaintiffs in the amounts of their individual overpayments as stated in the M & A model, as well as interest in the amount of six percent (6%), the statutory rate of interest in Pennsylvania, on the respective amounts of overpayments beginning January 1, 2008.

10. A constructive trust arises where a person holding title to a property is subject to an equitable duty to convey it to another on the grounds that the person would be unjustly enriched if the person were permitted to retain it. A constructive trust may arise even though the acquisition of the property was not wrongful and a defendant’s intention was not ill conceived. The court focuses not upon intention, but upon the result of the unjust enrichment. The Court held that it would apply the equitable doctrine of constructive trust to ensure that the taxes erroneously retained by the Defendants would be repaid to the Plaintiffs.

11. The elements to a cause of action under the Local Tax Enabling Act are: (1) earned income taxes are not distributed to the appropriate political subdivision within one (1) year after receipt of those funds by a tax officer; (2) the aggrieved political subdivision presents a written demand on the tax officer or political subdivision seeking the return of the revenues attributable to the residents of the aggrieved political subdivision; and (3) the entity improperly retaining the tax revenues fails to remit the proper amount to the aggrieved political subdivision within thirty (30) days of the demand. The Court found that Plaintiffs established all of the necessary elements to prove a cause of action under the Local Tax Enabling Act and again directed the repayment of the overpaid taxes by the Defendants as indicated in the M & A model with legal interest as of January 1, 2008.

12. Civil conversion requires an intentional deprivation of another’s right to property without the owner’s consent and lawful justification. The Court viewed the Plaintiffs’ theory of conversion as an attempt to create civil liability as a result of a defendant’s failure to settle a dispute, as Plaintiffs asserted that the elements of conversion accrued not when the Bureau inappropriately distributed tax funds, but when the report of M & A revealed the improper distributions. The Court stated that neither conversion nor any other tort imposes a remedy against a party for failing to comply with a settlement demand. As such, the Court found in favor of Defendants regarding the Plaintiffs’ claim for conversion.

13. The doctrine of unclean hands requires that one seeking equity must act fairly and without fraud or deceit regarding the controversy at issue. The application of the unclean hands doctrine to deny relief is within the discretion of the Court, which is free to decline to apply it if a consideration of the entire record indicates that an inequitable result will be reached in the event of its application.

14. The Court rejected Defendants’ assertion that Plaintiffs’ failure to oversee the Bureau, to reconcile its distributions with those of the Bureau and to determine the existence of a problem constitutes unclean hands precluding Plaintiffs’ recovery under its equitable claims.

15. The Court ruled in favor of Defendants and against the Bureau in Defendants’ claims in Negligence and violation of the Local Tax Enabling Act, as the director hired by the Bureau acted fraudulently and with willful disregard for the duties of his office and the Bureau was negligent in its oversight of Foltz in carrying out his duties.

16. The Court held that the seven (7) year statute of limitations set forth in the Local Tax Enabling Act had been tolled in accordance with the discovery rule and would not serve as a defense to Defendants’ claim against the Bureau for a violation of the Local Tax Enabling Act.

17. The Court held that the Political Subdivision Tort Claims Act did not bar the Defendants’ claims against the Bureau on the basis of immunity from liability as a local agency, as the Court explained that the Political Subdivision Tort Claims Act applies only in the context of tort litigation, the circumstances of this case would not serve the intention of the Political Subdivision Tort Claims Act of limiting governmental exposure and preserving the public treasury against the possibility of unusually large recoveries in tort cases and a provision of the Political Subdivision Tort Claims Act excludes its applicability cases in which an act of an employee of an agency constitutes willful misconduct.

18. In assessing Defendants’ remedies against the Bureau, the Court recognized that compensatory damages are damages sufficient to indemnify the injured party for the loss suffered. The Court also observed that consequential damages are losses that do not flow directly and immediately from the injurious act but that result indirectly from that act.

19. The Court rejected the Defendants’ request to recover the monies which they were overpaid by the Bureau as indicated by the M & A model as compensatory damages, as the Court reasoned that Defendants never should have received the overpaid funds in the first place and would not be harmed by being required to repay those funds.

20. The Court indicated that it would entertain a request from Defendants for consequential damages against the Bureau, as the distribution scheme that created the overpayments impacted Defendants in ways that transcend their obligations to repay the overpayments.

21. The Court recognized that while Defendants will be required to pay their own litigation-related expenses under the “American Rule” that requires each party to pay its own counsel fees regardless of the party who prevails at trial, the investigative fees and costs expended by Defendants prior to litigation fairly would be assessed against the Bureau.

L.C.C.C.P. No 2012-01222, Bradford H. Charles, Judge, July 15, 2015.

Thomas B. Schmidt, III, Esq., David J. Tshudy, Esq., Justin G. Weber, Esq., and Tucker R. Hull, Esq., for Plaintiffs

Scott T. Wyland, Esq., for Defendants

Howard L. Kelin, Esq., for Additional Defendant

IN THE COURT OF COMMON PLEAS OFLEBANON COUNTY, PENNSYLVANIA

CIVIL ACTION – LAW No. 2012-01222

CITY OF LEBANON, JONESTOWN BOROUGH, NORTH CORNWALL

TOWNSHIP, NORTH LEBANON TOWNSHIP, NORTH LONDONDERRY TOWNSHIP, NORTH LEBANON SCHOOL DISTRICT, PALMYRA AREA SCHOOL DISTRICT, SOUTH LEBANON TOWNSHIP, SOUTH LONDONDERRY TOWNSHIP, SWATARA TOWNSHIP, UNION TOWNSHIP, and WEST LEBANON TOWNSHIP,

Plaintiffs

v.

CORNWALL BOROUGH, HEIDELBERG TOWNSHIP, NORTH ANNVILLE TOWNSHIP, WEST CORNWALL TOWNSHIP, and BETHEL TOWNSHIP,

Defendants

v.

LEBANON COUNTY EARNED INCOME TAX BUREAU,

Additional Defendant

ADJUDICATION

AND NOW, this 15th day of July, 2015, after bench trial and in consideration of the parties’ Stipulation of Facts and all other information presented, the verdicts of this Court are as follows:

1. On Plaintiffs’ causes of action of unjust enrichment, constructive trust and a violation of the Local Tax Enabling Act, our verdicts will be as follows:

(a) In favor of Plaintiffs and against Cornwall Borough in the amount of $1,532,182.20 plus interest to be computed from July 1, 2015;

(b) In favor of Plaintiffs and against North Annville Township in the amount of $399,350.21 plus interest to be computed from July 1, 2015;

(c) In favor of Plaintiffs and against Heidelberg Township in the amount of $1,111,904.70 plus interest to be computed from July 1, 2015;

(d) In favor of Plaintiffs and against West Cornwall Township in the amount of $187,903.23 plus interest to be computed from July 1, 2015;

(e) In favor of Plaintiffs and against Bethel Township in the amount of $102,328.68 plus interest to be computed from July 1, 2015.

2. On Plaintiffs’ cause of action for conversion, we find in favor of Defendants and against Plaintiffs.

3. With respect to the Defendants’ claim against Additional Defendant Lebanon County Earned Income Tax Bureau, we find in favor of the Defendants and against the Additional Defendant based upon the Defendants’ theories of negligence and a violation of the Local Tax Enabling Act. As a remedy, the Defendants will be entitled to recover pre-litigation fees and expenses. The Defendants shall submit to all opposing parties and this Court an itemized list of all pre-litigation costs and expenses which it seeks to recover. This itemized list is to be submitted within 10 days. Within 10 days thereafter, any other party may object to the amounts claimed by the Defendants. If a dispute exists, we reserve the right to schedule another hearing to determine the amount of the dispute. If no dispute exists, we will award Defendants the amount of pre-litigation fees and costs which it seeks.

4. All fees charged by Forensic Accountant Dennis Houser are to be divided equally between the parties.

BY THE COURT:

BRADFORD H. CHARLES, J.

TABLE OF CONTENTS

I. INTRODUCTION AND GLOSSARY

II. SUMMARY OF STIPULATED FACTS

III. SUMMARY OF TRIAL TESTIMONY

IV. DISCUSSION

A. M&A Analysis

B. General Principles of Equity

C. Unjust Enrichment

D. Constructive Trust

E. LTEA

F. Conversion

G. Unclean Hands

H. PLAINTIFFS’ Remedy

I. Responsibility of BUREAU

J. BUREAU’s Defenses

(1) Statute of Limitations

(2) Political Subdivision Tort Claims Act

K. DEFENDANTS’ Remedies Against BUREAU

V. CONCLUSION

APPEARANCES:

Thomas B. Schmidt, III, Esquire For Plaintiffs

David J. Tshudy, Esquire

Justin G. Weber, Esquire

Tucker R. Hull, Esquire

PEPPER HAMILTON, LLP

Scott T. Wyland, Esquire For Defendants

SALZMANN HUGHES, P.C.

Howard L Kelin, Esquire For Additional Defendant

KEGEL KELIN ALMY & LORD LLP

ADJUDICATION AND OPINION BY CHARLES, J., July 15, 2015

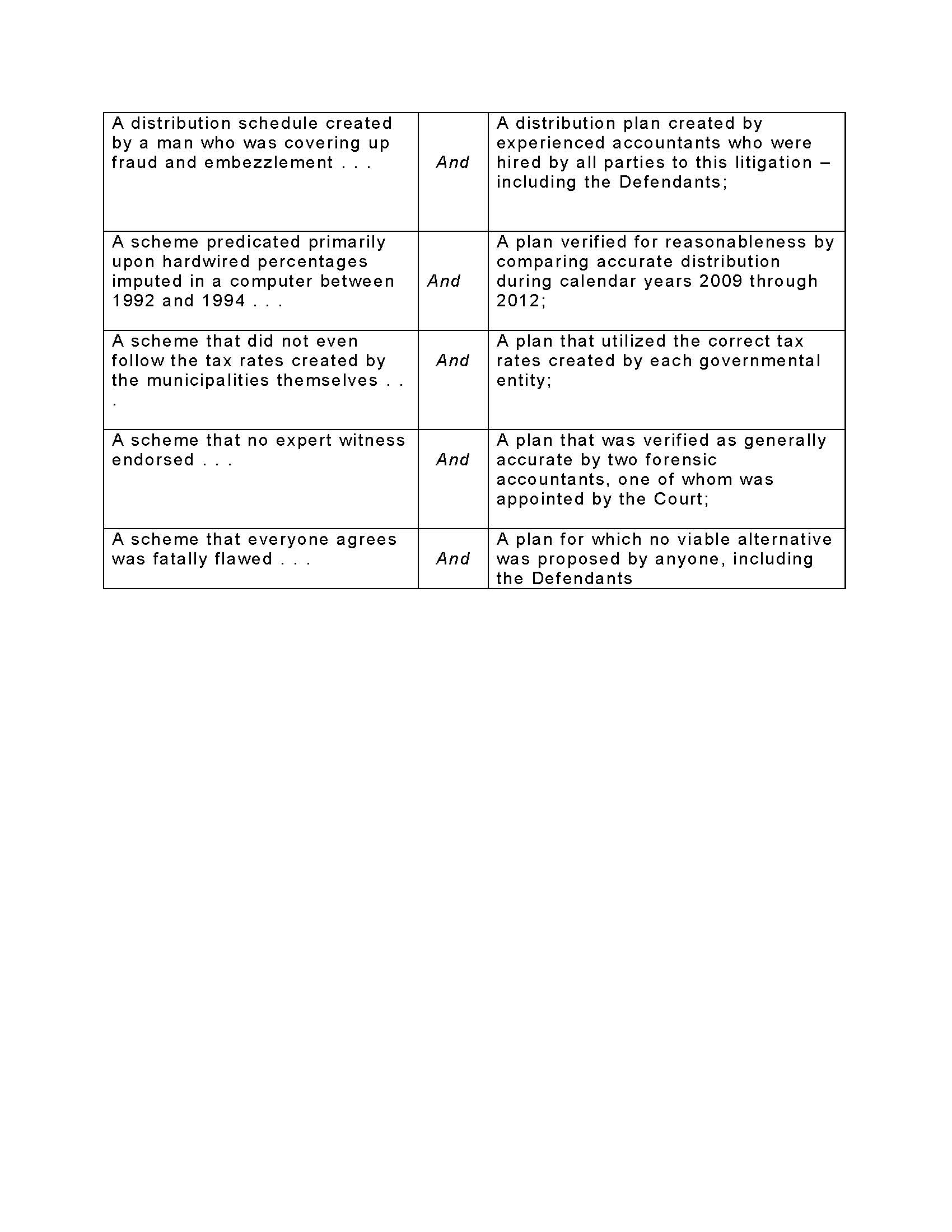

Given a choice between rough but imperfect justice and gross inequity created in part by corruption, we will choose the former every time. Before us today is the question of how millions of dollars of tax money should be distributed between local school districts and municipalities. Our choices are between [click on image to expand]:

When faced with the alternatives articulated above, our choice is crystal clear. For reasons that we will articulate in more detail within the body of this Opinion, we will redistribute over three million dollars in tax revenue plus interest from municipalities that were overpaid by the corruption-ridden former Earned Income Tax Bureau of Lebanon County to taxpayers in municipalities who were shortchanged for a period of four years.

I. INTRODUCTION AND GLOSSARY

This dispute over distribution of tax monies is as complicated as it is notorious in Lebanon County. The above-captioned lawsuit is only one of several that stemmed from the corruption and mismanagement of the former Earned Income Tax Bureau of Lebanon County when it was led by Donald Foltz. In 2007, the Bureau learned that Mr. Foltz had embezzled over $800,000.00 in taxpayer money. After Mr. Foltz was terminated from his job and committed suicide, a proverbial train of enlightenment gathered steam. It eventually impacted the Bureau’s bonding agency, Foltz’ widow, the BUREAU’s Bank, several accounting firms, numerous local officials and, at least indirectly, every taxpayer within Lebanon County. After months of trying to sort out what one lawyer characterized as a “true mess,” the citizens of Lebanon County learned that the monies distributed by the Bureau between 2004 and 2007 may not have been distributed in a manner that matched the intent of the tax ordinances passed by each school district and municipality. This epiphany was what led to the litigation now before this Court.

Fortunately, the parties to this dispute have been represented by capable and collegial counsel. Recognizing that there was consensus with respect to much of the underlying information relevant to our decision, counsel agreed to two stipulations of fact totaling 26 pages. To supplement those stipulations, we heard testimony in Court from eight witnesses. One of these witnesses was a forensic accountant appointed by the Court to render an independent opinion. We will begin our analysis by summarizing the parties’ stipulations and the testimony presented in Court. Thereafter, we will conduct an analysis of the primary issue before us – how the disputed tax dollars should be distributed. Finally, we will analyze the parties’ legal arguments and will render a final decision.

Before we embark upon the above, we perceive that it would be helpful to create a glossary of sorts. The monikers we will be employing to describe various individuals and entities throughout this opinion will be as follows:

PLAINTIFFS – Various Lebanon County school districts and municipalities that allege that they were underpaid tax money between 2004 and 2007.

DEFENDANTS – Five Lebanon County Municipalities that Plaintiffs believe were overpaid tax money between 2004 and 2007.

BUREAU – The now-defunct Lebanon County Earned Income Tax Bureau that was responsible for distributing tax money between 2004 and 2007.

FOLTZ – Donald Foltz, who was the former Executive Director of the Bureau, was discovered to have embezzled money between 2004 and 2007. His job was terminated in March of 2007. Several weeks later, he committed suicide.

M&A – McKonly & Asbury, which was a firm hired by the Bureau with the approval of all of its constituencies. M&A was charged with the responsibility of trying to recreate an appropriate tax distribution model for the years 2004 through 2007.

MORAN – Nancy Moran was a consultant hired by the Bureau to serve as Interim Director following the termination of Foltz’ employment. Moran served as the Director of the Bureau between April of 2007 and the time it finally became defunct in late 2008.

BOWERCRAFT – Samuel Bowercraft is a principal at M&A who is trained in data analytics. Mr. Bowercraft was the individual employed by M&A who was primarily responsible for developing the opinions and report of M&A.

SMITH – Dana Trexler Smith is a forensic accountant who was employed by Plaintiffs to conduct an analysis of the methodology employed by M&A.

DUFFUS – David Duffus is a forensic accountant who was hired by the ELCO School District to analyze and critique the methodology employed by M&A.

FREEH – Cheri Freeh is an accountant hired by Defendants to analyze and critique the methodology employed by M&A.

HOUSER – Dennis Houser is a forensic accountant who was appointed by the Court to conduct an independent analysis and critique of the methodology employed by M&A.

HOFFMAN – Rebecca Hoffman is a former employee of the Bureau.

GRUMBINE – Cheri Grumbine is the township manager of North Lebanon Township. After M&A communicated its findings, Ms. Grumbine developed a plan by which allegedly overpaid school districts and municipalities could repay alleged underpaid municipalities and school districts over an extended period of time. This plan later became known as the “Grumbine Plan.”

KEYSTONE – The Keystone Collections Group is a company that was hired in late 2008 to collect earned income tax and distribute it accurately to local political subdivisions.

LTEA – The LTEA is the Local Tax Enabling Act

II. SUMMARY OF STIPULATED FACTS

The BUREAU was created in 1967 through a “joint agreement” that was approved by all Lebanon County School Districts and Municipalities. The purpose of the BUREAU was “to collect and distribute earned income tax payments ….” During its existence, the BUREAU was governed by a six-person executive committee comprised of one representative from each of the county’s six school districts. In 1987, FOLTZ was hired to serve as the BUREAU’s Executive Director. FOLTZ designed and implemented the system that was used to distribute tax revenues to school districts and municipalities.

In 2006, the BUREAU’s Executive Committee began an investigation into the administration of the BUREAU. As part of the investigation, the committee retained the accounting firm of Boyer and Ritter to review the BUREAU’s internal controls. Boyer and Ritter issued a report in early March of 2007. On the same day that the report was issued, FOLTZ was placed on administrative leave. One week later, on March 14, 2007, FOLTZ’ employment with the BUREAU was terminated. On March 30, 2007, FOLTZ committed suicide.

Shortly after FOLTZ was relieved of his duties, the BUREAU discovered that money had been embezzled. It was learned that between 2002 and 2006, FOLTZ deposited $895,676.15 of tax revenues into an “off books” account to which only FOLTZ had access. Of this amount, FOLTZ removed $811,000.00 for his own use and benefit. The remaining $80,000.00 that had been deposited into the fraudulent account was recovered by the BUREAU. Later, the BUREAU’s bonding agency reimbursed the BUREAU for $801,000.00 that FOLTZ had stolen.

MORAN was hired on a contract basis to serve as Interim Executive Director of the BUREAU following FOLTZ’ termination. By the end of 2007, MORAN issued a report to the BUREAU’s Executive Committee expressing a concern that tax revenues for the time period between 2004 and 2007 had not been distributed properly. MORAN identified three primary concerns:

(1) Incorrect tax distribution percentages were inputted into the BUREAU’s computer system and were used to distribute tax revenue;

(2) FOLTZ “rounded up” or “rounded down” tax distributions that were determined in accordance with the BUREAU’s computer system;

(3) Incorrect tax rates were inputed into the computer system with respect to three school districts and three local municipalities.

As a result of MORAN’s report, all Lebanon County school districts and municipalities agreed that a more detailed investigation should be launched to determine whether overpayments or underpayments were made during the years 2004 through 2007. In July of 2008, all Lebanon County school districts and municipalities agreed to hire M&A to conduct an analysis of the BUREAU’s tax distribution decisions between 2004 and 2007.

The parties have stipulated that “it was impossible for M&A to recreate the necessary tax data using BUREAU records alone, because the BUREAU did not possess adequate and accurate records of individual taxpayer tax payments for the relevant years.” (¶ 75 of Stipulation). M&A learned that many tax returns no longer existed; BUREAU employees reported that “files and documents were untidy, disorganized and sometimes missing, and there was shredding of documents….” (¶ 78 of Stipulation).

M&A decided to obtain Pennsylvania Department of Revenue data for each taxpayer in Lebanon County. The Department of Revenue possessed a database that identified taxpayers by Social Security numbers and annual compensation. Using data from the Department of Revenue, M&A embarked on analysis to discern whether municipalities had been underpaid or overpaid between 2004 and 2007. After completing its analysis, M&A issued a report on March 17, 2010. M&A concluded that the following school districts and municipalities were underpaid tax money for the years 2004 through 2007:

|

Annville Township |

$ 11,996.40 |

|

City of Lebanon |

$1,447,958.54 |

|

Jonestown Borough |

$ 166,503.09 |

|

North Cornwall Township |

$ 315,164.25 |

|

North Lebanon Township |

$ 822,264.07 |

|

North Londonderry Township |

$ 587,268.05 |

|

Northern Lebanon School District |

$ 107,236.24 |

|

Palmyra Area School District |

$ 859,018.57 |

|

South Lebanon Township |

$ 459,635.34 |

|

South Londonderry Township |

$ 529,205.07 |

|

Swatara Township |

$ 166,457.74 |

|

Union Township |

$ 159,455.69 |

|

West Lebanon Township |

$ 62,135.66 |

In addition, M&A determined that the following school districts and municipalities were overpaid money during the same years:

|

Annville-Cleona School District |

$ 500,523.00 |

|

Bethel Township |

$ 70,571.51 |

|

Cleona Borough |

$ 43,806.82 |

|

Cornwall Borough |

$1,056,677.45 |

|

Cornwall-Lebanon School District |

$ 384,926.28 |

|

East Hanover Township |

$ 186,941.80 |

|

Eastern Lebanon School District |

$1,171,005.50 |

|

Heidelberg Township |

$ 766,830.89 |

|

Jackson Township |

$ 47,838.69 |

|

Lebanon School District |

$ 326,089.11 |

|

Millcreek Township |

$ 941.76 |

|

Mt. Gretna Borough |

$ 219,053.91 |

|

Myerstown Borough |

$ 44,387.37 |

|

North Annville Township |

$ 275,413.94 |

|

Palmyra Borough |

$ 129,669.20 |

|

Richland Borough |

$ 26,312.78 |

|

South Annville Township |

$ 313,720.28 |

|

West Cornwall Township |

$ 129,588.44 |

Following the publication of M&A’s report, 13 of the 18 political subdivisions in Lebanon County identified as “overpaid” agreed to return their overpayments to the school districts and municipalities who were underpaid. The DEFENDANTS did not agree. The following chart represents the amount of money that M&A’s report identified as being overpaid to the five DEFENDANTS:

|

Cornwall Borough |

$1,056,677.45 |

|

Heidelberg Township |

$ 766,830.89 |

|

North Annville Township |

$ 275,413.94 |

|

West Cornwall Township |

$ 129,588.44 |

|

Bethel Township |

$ 70,571.51 |

By a letter dated December 23, 2011, counsel for PLAINTIFFS contacted DEFENDANTS in order to demand payment of the alleged overpaid amounts that the DEFENDANTS retained. The DEFENDANTS declined to pay such amounts.

Beginning in the third quarter of 2008, all school districts and local municipalities agreed that future tax collection and distribution should be conducted by KEYSTONE. KEYSTONE immediately began collecting earned income tax money and distributing it to local municipalities and school districts.

The parties also stipulated that each of the DEFENDANTS received earned income tax disbursements of the following amounts:

1. Bethel Township

|

2004 |

$407,122.67 |

|

2005 |

$435,580.43 |

|

2006 |

$461,914.56 |

|

2007 |

$441,216.89 |

|

2008 |

$466,114.00 |

|

2009 |

$438,807.00 |

|

2010 |

$430,203.00 |

|

2011 |

$455,056.00 |

|

2012 |

$486,431.00 |

2. Cornwall Borough

|

2004 |

$683,660.85 |

|

2005 |

$723,022.42 |

|

2006 |

$772,381.13 |

|

2007 |

$742,348.97 |

|

2008 |

$675,582.77 |

|

2009 |

$443,018.49 |

|

2010 |

$511,695.13 |

|

2011 |

$511,102.69 |

|

2012 |

$577,762.69 |

3. West Cornwall Township

|

2004 |

$220,096.58 |

|

2005 |

$231,285.34 |

|

2006 |

$245,726.20 |

|

2007 |

$230,519.51 |

|

2008 |

$232,582.00 |

|

2009 |

$196,618.00 |

|

2010 |

$202,095.00 |

|

2011 |

$207,171.00 |

|

2012 |

$221,247.00 |

4. Heidelberg Township

|

2004 |

$505,148.23 |

|

2005 |

$534,148.23 |

|

2006 |

$570,700.86 |

|

2007 |

$567,498.21 |

|

2008 |

$532,957.00 |

|

2009 |

$343,463.00 |

|

2010 |

$333,289.00 |

|

2011 |

$327,976.00 |

|

2012 |

$383,862.00 |

5. North Annville Township

|

2004 |

$272,049.29 |

|

2005 |

$290,270.39 |

|

2006 |

$312,991.67 |

|

2007 |

$257,120.42 |

|

2008 |

$234,600.00 |

|

2009 |

$230,724.00 |

|

2010 |

$253,520.00 |

|

2011 |

$240,219.00 |

|

2012 |

$245,305.00 |

III. SUMMARY OF TRIAL TESTIMONY

BOWERCRAFT was the first witness to testify. BOWERCRAFT had training and experience in what he called “data analytics.” BOWERCRAFT was an employee of M&A and was primarily responsible for conducting M&A’s analysis of Lebanon County tax distributions between 2004 and 2007. Together with BOWERCRAFT, three other “team members” of M&A worked on the project. Together the M&A “team” spent almost 500 hours working on an analysis of how monies were and should have been distributed in Lebanon County.

BOWERCRAFT testified that processes and controls governing tax distribution during 2004 and 2007 were “totally lacking.” Based upon information provided by MORAN and employees at the BUREAU, M&A concluded that the tax revenue records of the BUREAU could not be relied upon. In other words, no accurate reconciliation of tax distribution could be conducted based exclusively upon the BUREAU’s records.

BOWERCRAFT and his team developed an analytical model to discern how tax revenue should have been divided between 2004 and 2007. That analytical model was as follows:

(1) Taxpayer compensation would be derived from Pennsylvania Department of Revenue records;

(2) Taxpayer residence would be derived from the BUREAU’s records;

(3) An analysis would be conducted of the degree to which the BUREAU’s residence records and the Department of Revenue’s compensation records could be “matched.”

(4) If the “match” was deemed to be representative, the Department of Revenue’s income data would be used to determine what percentage of earned income tax revenue should be distributed to each local agency using correct tax rates.

BOWERCRAFT communicated the analytical model developed by M&A with the BUREAU’s Board of Directors. No evidence was presented that anyone dissented to M&A’s proposed methodology. M&A thus embarked on a one-year project to employ the model that was outlined above. M&A’s data analysis was not completed until early 2010.

BOWERCRAFT testified that with the assistance of local officials, M&A was able to obtain compensation records from the Department of Revenue broken out by Social Security numbers of taxpayers. BOWERCRAFT testified that M&A was able to match 88% of state revenue records with local tax role documentation. Of more importance to BOWERCRAFT was the fact that there was a 95% “revenue capture.” In other words, BOWERCRAFT testified that 95% of revenue from Social Security numbers identified by the Department of Revenue matched Lebanon County residents. In real dollars, BOWERCRAFT testified that M&A “matched” 8.5 billion dollars in revenue to local Lebanon County taxpayers. M&A determined that this was “good enough” to create a viable analysis of whether or to what extent each Lebanon County local government agency was overpaid or underpaid. The analysis that was therefore derived was summarized by BOWERCRAFT in a table marked as Table 6 to Exhibit 3. A copy of that table is as follows [click on image to expand]:

After M&A published its findings, but before the trial, M&A undertook to compare its findings with actual tax distributions made by KEYSTONE. BOWERCRAFT testified that KEYSTONE distributed tax revenue using original tax returns, locally-generated documentation and a correct methodology. BOWERCRAFT viewed the KEYSTONE disbursements as being the most accurate gauge of how Lebanon County local income tax should be distributed. Using these accurate figures, BOWERCRAFT created graphs representing KEYSTONE’s actual disbursements and M&A’s calculations. BOWERCRAFT testified that the M&A calculations for 2004 through 2007 aligned very closely with KEYSTONE’s correct actual disbursements between 2009 and 2011.

On cross-examination, BOWERCRAFT acknowledged that M&A’s analysis was predicated upon figures that were derived using the Commonwealth of Pennsylvania’s definition of income. BOWERCRAFT also acknowledged that there are differences between the state’s definition of what is taxable and local agencies’ definitions of what is deemed to be taxable. Of most note is the fact that S corporation profits are includable as income on state returns but are excludable on local income tax returns. BOWERCRAFT acknowledged that this difference could help explain why 5% of state revenues were not “captured” in M&A’s analysis.

BOWERCRAFT also acknowledged that the BUREAU did not properly disburse amounts paid by wage earners who worked but did not live in Lebanon County. By law, local income tax deducted from non-resident workers should have been distributed to the counties where those non-resident workers resided. The BUREAU did not do this between 2004 and 2007, and M&A made no accommodation in its calculations for this sort of non-resident taxation.

BOWERCRAFT also admitted on cross-examination that neither the BUREAU nor KEYSTONE adopted M&A’s percentages for purposes of distributing 2008 or future local earned income tax. Likewise, BOWERCRAFT acknowledged that M&A never undertook to determine whether the “size of the tax pie” collected by the BUREAU was correct or incorrect; M&A’s sole purpose was to determine how the pie should have been divided between all of the BUREAU’s local governmental constituencies.

The second witness at trial was forensic accountant Dana Trexler Smith. SMITH was hired by the PLAINTIFFS to conduct a litigation-focused evaluation of M&A’s methodology. SMITH was asked whether the M&A methodology could be relied upon “to a reasonable degree of accounting certainty.”

In describing the purpose of an accounting reconstruction, SMITH characterized the goal as determining “what should distributions have looked like in a perfect world.” SMITH acknowledged that determining what a “perfect world” would look like in this case was impossible given the disarray of the BUREAU and its records. SMITH opined that the “next best source of information” that could be used to determine taxable income was the Department of Revenue records that were reviewed by M&A.

SMITH acknowledged that the local definition of income excluded S corporation earnings that would have been included in the Department of Revenue documentation. However, she stated that federal statistics reveal that S corporation income is only 3% of the total aggregate taxable income in the United States.

SMITH corroborated BOWERCRAFT’s description of M&A’s 95% compensation match as being “more important” than the 88% records match. However, she classified either match as complying with a “reasonable degree of accounting reconstruction certainty.” She also concurred with BOWERCRAFT’s testimony that KEYSTONE’s actual distribution amounts between 2009 and 2011 supported the accuracy of M&A’s calculated distribution percentages. SMITH stated: “The fact that M&A figures aligned with KEYSTONE figures told me that M&A figures were reasonable.”

Like BOWERCRAFT, SMITH acknowledged on cross-examination that M&A’s calculated percentages may not have been completely accurate. She acknowledged that the BUREAU’s decision not to distribute income to other counties for non-resident workers probably overstated the BUREAU’s distributions by 2% annually. She also acknowledged that the amount that FOLTZ embezzled – $811,000.00 – while less than 1% of the total amount distributed by the BUREAU, nevertheless also resulted in an overstatement of the gross amount of monies distributed by the BUREAU between 2004 and 2007. On the other hand, SMITH emphasized that M&A’s role was to determine percentages of distribution, not to verify whether the BUREAU distributed the correct aggregate amount to its constituencies between 2004 and 2007.

SMITH indicated that the BUREAU was riddled with “known fraud” and that fraud has “tentacles” that affect all aspects of recordkeeping. SMITH referenced the systematic destruction of records by FOLTZ and concluded that state Department of Revenue compensation records would be far more accurate than any incomplete analysis of existing BUREAU records. In addition, the DEFENDANTS’ counsel asked extensive questions of SMITH with respect to M&A’s decision to use the BUREAU’s records for residential purposes but not for income purposes. SMITH indicated that she believed that local school districts “vetted” the residency data maintained by the BUREAU, and this afforded additional verifiability with respect to the BUREAU’s residency data that would not have existed with respect to incomplete revenue data.

The Court questioned SMITH with respect to her opinion that the 88% records “match” and the 95% revenue “match” were within a reasonable degree of certainty with respect to accounting reconstruction. She described the 95% revenue match as “absolutely within” any variance standard that could be utilized. She also stated that the 88% records match was “still pretty good.” She testified that when an accounting reconstruction is completed, a 20% variance between known and presumed data (i.e., 80% verified and 20% not) would still be reasonable.

The next witness presented at trial was David Duffus. DUFFUS is a Certified Forensic Accountant who works for a firm in the Pittsburgh area. DUFFUS was originally hired by the ELCO School District to undertake a critique of the M&A evaluation. At the risk of oversimplification, DUFFUS was not critical of M&A’s decision to use Department of Revenue data in its reconstruction, but he was critical of M&A’s failure to test and verify the data: “M&A relied upon data that was not tested in any meaningful way.”

Unlike SMITH, DUFFUS characterized the number of tax records that were not “matched” between the Department of Revenue and the BUREAU as “very high,” especially in 2007. He opined that much more could have been done to verify the accuracy of the BUREAU’s residency records. Acknowledging that M&A did randomly select 120 taxpayer records and independently verified that 119 of those taxpayers did live at the address reflected on the BUREAU roles, DUFFUS opined that the verification sample should have been much larger.

On cross-examination, DUFFUS acknowledged that he was not supporting the BUREAU’s distribution percentages that were utilized to divide tax revenue between 2004 and 2007. He acknowledged that those distribution figures were “likely incorrect.” He also acknowledged that when he wrote his report for ELCO, the actual tax distribution data from KEYSTONE was not available. DUFFUS stated “I wanted to see the KEYSTONE data. I thought it would be meaningful.”

Cheri Freeh was next to testify. FREEH is a principal in an accounting firm located in Quakertown, Pennsylvania. She is not a forensic accountant. By her own admission, FREEH is not qualified to conduct a financial reconstruction similar to the one undertaken by M&A. However, FREEH has a wealth of experience in auditing of tax collection agencies such as BUREAU. Moreover, FREEH has unique experience with respect to local government taxation. For two years, she served as President of the Pennsylvania Institute for Certified Public Accountants. She also served on the Governor’s committee for local taxation.

FREEH was hired by the DEFENDANTS to examine whether the Department of Revenue documents were the “proper data set to use.” She was also asked to provide guidance with respect to auditing of a tax collection agency such as the BUREAU.

FREEH testified that most tax collection agencies paid quarterly tax estimates and a final reconciliation at the end of each year. She stated that the BUREAU conducted no reconciliations at all between 2004 and 2007. Both tax collection agencies and the governmental entities to whom taxes are paid must conduct reconciliation audits.

FREEH emphasized that “in reality, most school districts and municipalities rely upon the reconciliation of the collection agency and its auditor.” She stated that it would be impossible for school districts and municipalities to conduct a comprehensive audit “because the tax collector – not the municipalities – had possession of the actual records.” FREEH repeated on multiple occasions during her testimony that a tax collection agency’s audit is expected to be more strenuous and detailed than any reconciliations conducted by local municipalities.

According to FREEH, audits are not generally designed to detect fraud. She acknowledged that someone who is smart and nefarious will probably be able to commit fraud and avoid detection by an auditor. FREEH specifically stated that the type of audit normally conducted by municipalities and school districts “probably would not detect the type of embezzlement conducted by FOLTZ.”

On the other hand, FREEH was critical of the BUREAU’s auditor. She stated that a tax agency auditor should have detected the fact that tax rates established by local agencies differed from the distribution schedule maintained on the BUREAU’s computer. The BUREAU’s auditor should also have detected the fact that the BUREAU’s distribution percentages had not been updated since 1994. In addition, FREEH would have expected that the BUREAU’s auditor would have noticed and questioned the disorganized and disheveled state of the BUREAU’s recordkeeping as described by MORAN and other witnesses. In summary, FREEH testified that she would have expected the BUREAU’s auditor to have discovered problems between 2004 and 2007.

In terms of the auditing process, FREEH described the various phases of a tax collection agency audit. Those stages are:

(1) Calculate materiality – No auditor expects perfection. However, the auditor should know at the outset of his/her engagement “at what level can we have an error and still give a clean bill of health.”

(2) Audit plan – The auditor must develop a plan to assess internal controls, verify whether procedures were routinely followed and detect areas of weakness.

(3) Expectation analysis – An auditor must develop an expectation of what the data should show based upon past data.

(4) Testing – It is not necessary for an auditor to look at each and every source document. However, a representative sample of source documents must be examined and cross-checked to ensure validity and reliability.

(5) Explaining variance – If there is any variance between actual testing and the expectation developed that exceeds the materiality percentage developed in step one above, that variance must be examined and explained before an auditor can approve the entity being audited.

FREEH testified that there are auditing checklists that are adopted by accountants as “industry standard.” She referenced form ALGCX2.1 published by Thompson-Reuters PPC as one such form. FREEH testified that using these checklists can assist an auditor in determining what is and is not a “material variance.” For an entity like the BUREAU which processed between 90 and 100 million dollars in tax payments over four years, FREEH stated that anything over a $625,000.00 variance should be viewed as problematic. She then extrapolated that the 5 million dollar difference between the Department of Revenue income “captured” by M&A and the actual amount distributed by the BUREAU during the same time frame “exceeds the variance that would be approved by an auditor under any materiality standard.”

In her analysis, FREEH also attempted to develop an auditing expectation of the distribution percentages to which the BUREAU should have adhered between 2004 and 2007. She based her expectation on three components:

(1) The average distributions in the four years prior to 2004;

(2) The average distributions in the four years following 2007;

(3) A figure derived by multiplying census data by average weekly wage statistics to calculate an expected average per capita wage for each municipality and school district.

For reasons we will outline in more detail in the body of this Opinion, we did not find FREEH’s expectation analysis to be credible, and we will therefore not spend more time describing it.

During cross-examination, FREEH provided testimony that we found to be refreshingly candid. At one point, FREEH stated: “We are accountants. We can make numbers show whatever we want.” When discussing the plight of reconstructing the BUREAU’s appalling lack of verifiable revenue information, FREEH stated: “No one can provide a perfect answer. We are all giving estimates. The question is…which is the best estimate?”

Rebecca Hoffman worked for the Bureau between July of 1990 and September of 2008. She described FOLTZ as a dictatorial boss who demanded compliance and punished initiative. The picture painted by HOFFMAN of life at the BUREAU under FOLTZ was horrifying. HOFFMAN stated:

(1) When asked about recordkeeping by BUREAU employees, HOFFMAN responded rhetorically: “Have you ever seen the television show ‘Hoarders’? That is what it looked like.”

(2) When HOFFMAN gave FOLTZ computer reports reflecting how money should be distributed to various municipalities and school districts, he would adjust the figures. (See Exh. 19). His changes were “totally random.”

(3) Sometimes, FOLTZ would even physically confiscate a check before it was sent and demand that a new check in a different amount be written. Once again, there was no apparent or stated reason for this conduct.

(4) Several school districts would call and complain about the amount of their distribution. FOLTZ would be angered by these telephone calls. However, sometimes the amounts of the checks to these entities would be altered. HOFFMAN got the impression “the dog that barked the loudest got the benefit of changes in checks.”

(5) HOFFMAN eventually came to the conclusion that “there was no rhyme or reason to anything that was done.” To protect herself, HOFFMAN began making photocopies of documents whenever FOLTZ would alter computer print-outs or demand that check amounts be changed.

(6) If employees questioned FOLTZ, he would become quite angry. HOFFMAN observed that people who would have been in a position to perceive that FOLTZ was covering up his theft were paid monetary bonuses. Other hardworking employees were not paid such bonuses.

(7) FOLTZ kept boxes of records in his own office and refused to permit anyone to work on those records. On occasion, FOLTZ would also bring in an outside company to shred documents.

MORAN is a consultant who works for a company which provides interim CEOs for entities in transition. She earned a Master’s Degree in Accounting and a Master’s of Business Administration at Northeastern University. She was contacted by the BUREAU’s Board of Directors in March of 2007, and she agreed to undertake the responsibility to serve as Interim CEO. She then added with a wry smile: “I did not see the place before I agreed.”

MORAN described an environment at the BUREAU that was “in complete disarray.” She described the office as overcrowded, messy and completely disorganized. She stated that some employees were using Xerox boxes as work space. To compound these problems, the BUREAU’s computer system was antiquated; “it was DOS-based. I did not even know at the time that people still used DOS-based computers.”

One of the first things that MORAN discovered was that extra-payroll compensation was paid by FOLTZ. MORAN stated that three BUREAU employees received “five figure” compensation outside the BUREAU’s normal payroll. In addition, five to ten additional “home workers” were paid “compensation” for additional “work” that these individuals performed at home. MORAN was forced to prepare ex post facto W-2 and 1099 tax forms for each of these “workers.” At the direction of the BUREAU’s insurance company, all employees who had received “extra-payroll compensation” were terminated. One of the employees who received additional compensation resigned. Before she did so, she was caught attempting to place spyware on MORAN’s computer.

MORAN also quickly learned that FOLTZ had not paid distributions to out-of-county tax bureaus for non-resident tax income that was collected by the BUREAU. According to Exhibit 21, 1.95 million dollars was owed by the BUREAU to out-of-county governmental entities as of November 13, 2007.

MORAN also learned that the BUREAU had not been distributing tax money in accordance with the accurate tax rates adopted by local school districts and municipalities. By the end of 2007, MORAN advised the BUREAU’s Board of Directors that she believed tax money had been improperly distributed among the BUREAU’s various constituencies. She therefore recommended that an investigation be conducted to compare what had actually occurred and what should have occurred. Everyone agreed and M&A was eventually hired.

During the middle of MORAN’s tenure, it became obvious that the BUREAU would no longer be able to continue in a tax collection role. MORAN stated: “Trust in the BUREAU had been compromised. There was too much to recover from.” As a result, MORAN assisted in the selection of a new tax collection entity. MORAN testified that KEYSTONE was particularly impressive because it possessed “superior technology” and would be able to accurately discern how much money should be paid and to whom.

HOUSER is a forensic accountant who practices in Lebanon County. On April 7, 2015, this Court exercised its authority under Pa.R.Ev. 706 and appointed HOUSER as an independent accountant. We asked HOUSER to evaluate the process employed by M&A to determine overpayments and underpayments. In HOUSER’s own words:

In accordance with the Court’s order dated April 7, 2015, my evaluation was limited to examining the methodology employed by M&A and expressing an opinion regarding the fairness of the findings developed by M&A. I have not rendered an opinion with respect to specific amounts by which the parties may have been over or underpaid.

HOUSER testified that he reviewed hundreds of pages of documents provided by the Court and all parties. Included among these documents were all of the reports authored by M&A, the report submitted to ELCO School District by DUFFUS, an affidavit from BOWERCRAFT and the deposition of FREEH. In addition, this Court caused the testimony of HOFFMAN at trial to be transcribed, and a copy of that transcript was provided to HOUSER before he testified in Court.

HOUSER acknowledged that the methodology employed by M&A resulted in calculations that were imperfect. He acknowledged that the state and local definitions of income varied, and that M&A’s evaluation of only 120 local tax returns as a “control” could have been expanded. Nevertheless, HOUSER concluded that M&A’s findings were fair and reasonable. In his report, HOUSER stated: “It is my opinion with a reasonable degree of accounting and professional certainty that the methodology employed by M&A, and its related findings, while admittedly imprecise, are fair and reasonable based upon all facts known to the parties.”

IV. DISCUSSION

The parties have presented us with legal and factual arguments that require discussion. However, we recognize that there is one overriding factual question that will impact all others before us – Whether the M&A analysis of overpayments and underpayments is reasonable and credible? We will therefore begin by addressing this fundamental dispute that was hotly contested by the parties. Thereafter, we will address all of the parties’ numerous factual and legal arguments.

A. M&A Analysis

Notwithstanding all of the punches thrown by the DEFENDANTS at M&A’s evaluation, never once did the DEFENDANTS proffer an alternative distribution proposal. By asking this Court to continue the status quo, the DEFENDANTS have essentially asked us to endorse the scheme of distribution for which FOLTZ was the architect. We would find such a result unconscionable for many reasons, including the following:

(1) FOLTZ was a criminal who systematically pilfered hundreds of thousands of dollars of taxpayer money. FOLTZ had a vested interest in covering up his theft, and he employed fraud and deception to do just that. FOLTZ was the antithesis of trustworthy and we categorically reject his work product as worthy of our endorsement.

(2) The scheme of distribution created and implemented by the BUREAU did not even employ the correct tax rates for four school districts and municipalities. Stated differently, the distribution of tax money by the BUREAU did not comport with the will of the people who, through their elected representatives, determined how income should be taxed at a local level.

(3) The percentages of tax money distributed to each municipality were inputted into the BUREAU’s computer between 1992 and 1994 and were never altered thereafter. In a multitude of ways, Lebanon County evolved between 1994 and 2007. Some municipalities and school districts grew dramatically, while others constricted both in terms of population and economic output. This was not reflected in the BUREAU’s hard-wired distribution percentages.

(4) FOLTZ either intentionally or carelessly neglected to distribute non-resident worker local income tax to out-of-county agencies. The parties stipulated that almost 2 million dollars in non-resident earned income tax was not paid to the entities who were entitled to receive said funds.

(5) FOLTZ unilaterally and arbitrarily altered computer-generated tax distribution schedules so that the final distribution did not even comport with the hard-wired percentages imputed into the computer system. Although FOLTZ took the reason for these arbitrary alterations with him to his grave, HOFFMAN perceived that distributions were sometimes changed “because the dog that barks the loudest gets the most attention.”

(6) FOLTZ sometimes altered the computer-generated schedules of distribution to create “rounded” numbers that were not in accord with the actual hard-wired percentages inputted into the AS-400 computer program.

(7) When MORAN was hired by the BUREAU, she learned that FOLTZ had paid off-payroll bonuses and financial compensation to some BUREAU employees and outside individuals with no ties to the BUREAU. FOLTZ authorized the payment of tens of thousands of dollars without the knowledge of the BUREAU’s Board of Directors and without even the issuance of a Federal W-2 or 1099 statement.

(8) FOLTZ did not reconcile his year-end tax distributions. In fact, he had no incentive to do so given that he was concealing his own theft of taxpayer funds.

(9) The BUREAU utilized an antiquated DOS-based computer system that MORAN described as inadequate for the task it was asked to undertake. In addition, the recordkeeping system employed by the BUREAU was inefficient, inconsistently applied, and sometimes ignored altogether.

(10) No meaningful audits were performed of the BUREAU’s work between 2004 and 2007. In 2006 and 2007, the BUREAU continued to distribute tax monies without any audit whatsoever. For 2004 and 2005, we conclude based upon the information presented at trial that the BUREAU’s auditors performed their assignment in a manner that was grossly negligent and wholly inadequate. In essence, we determine that the work product of the BUREAU between 2004 and 2007 was unsupported by any viable internal controls or external audits.

We conclude based upon all of the above that adopting the DEFENDANTS’ position in favor of the status quo would have the effect of approving a distribution scheme by BUREAU that is completely and utterly unworthy of approval. Stated bluntly, the BUREAU’s distribution of tax money between 2004 and 2007 was the product of corruption, mismanagement, malfeasance, neglect and lack of oversight. None of the above are descriptive words that we wish to have associated with a verdict that seeks to effectuate justice. We therefore categorically reject the BUREAU’s actual distribution of funds between 2004 and 2007 as any benchmark of how taxpayer monies should have been allocated between 2004 and 2007.

Having reached the above conclusion, we must still evaluate whether the distribution scheme proffered by M&A can or should form the basis of a verdict in favor of PLAINTIFFS. As we do so, we cannot ignore the reality that M&A was confronted with “a true mess” when it undertook to conduct its analysis. Given the fraud perpetrated by FOLTZ, the fact that records were stored in a haphazard manner, and the fact that multiple witnesses reported that FOLTZ systematically shredded a multitude of records and tax returns to cover his own trail, it was simply impossible for M&A – or anyone else – to conduct a completely accurate reconstruction of how tax monies should have been distributed between 2004 and 2007. Given that perfection was simply not possible, the question we are required to answer is: “Was M&A’s effort good enough?” For the following reasons, we hold that it was:

(1) M&A was hired to conduct its analysis by all Lebanon County school districts and municipalities, including the DEFENDANTS. BOWERCRAFT testified that once he and his team identified a methodology – but before the results of that methodology could be known – he spoke with representatives of the local municipalities to explain and then discuss how the analysis would be conducted. There is no evidence that anyone objected to M&A’s analytical process until after it was discovered that some entities had been overpaid.

(2) SMITH is a forensic accountant who has conducted data reconstruction for 18 years. She testified to a reasonable degree of accounting certainty that the M&A methodology was appropriate and generated a “proxy result” that would be within a reasonable variance to “what the info would have looked like in a perfect world.” We found SMITH’s testimony to be credible.

(3) HOUSER was an independent expert appointed by the Court. When it became apparent during pretrial proceedings that several highly-qualified accountants had rendered differing opinions with respect to M&A’s methodology, this Court decided to invoke the authority granted to it under Pa.R.Ev. 706 to solicit assistance from an independent accountant. Dennis Houser of Financial Forensic Consultants, LLC has been a Certified Public Accountant since 1977 and a Certified Fraud Examiner since 1992. He is familiar with how financial reconstruction is undertaken. Because HOUSER approached the task of analyzing M&A’s analysis from a non-partisan perspective, we have afforded his opinion with significant weight. HOUSER concluded: “It is my opinion with a reasonable degree of accounting and professional certainty that the methodology employed by M&A and its related findings, while admittedly imprecise, are fair and reasonable based upon all facts known to the parties.” (HOUSER’s Report at pg. 18).

(4) When M&A conducted its analysis, it was able to “capture” 95% of revenue compensation by matching it with local records. In other words, M&A was able to match 95% of the compensation figure obtained from the Department of Revenue with local taxpayers. Both HOUSER and SMITH described this 95% compensation match as “extremely high.”

(5) For nearly one full day, we listened to BOWERCRAFT testify about his methodology. In the process, we watched BOWERCRAFT respond to the criticisms hurled by the DEFENDANTS. The more we listened to BOWERCRAFT’s testimony, the more we were impressed by his grasp of data analytics and the application of his expertise to the difficult assignment of reconstructing how taxes should have been distributed in Lebanon County between 2004 and 2007. The bottom line is that we found BOWERCRAFT’s testimony to be credible.

(6) Although DUFFUS complained that M&A could and should have done far more to test and verify the raw data which it utilized, DUFFUS was not highly critical of the analytical process employed by M&A. Moreover, at the time DUFFUS completed his report for the ELCO School District, the KEYSTONE tax distribution data for 2009 through 2012 was not available. DUFFUS stated: “I wanted to see the KEYSTONE data. I thought it would be meaningful.” We agree with DUFFUS that the KEYSTONE calculation of tax distribution was an important piece of the reconstruction verification process, and DUFFUS’ self-admitted inability to examine such data causes us to view with skepticism the ultimate conclusion he communicated to the ELCO School District.

(7) We found FREEH to be refreshingly candid in her testimony. We chuckled at the irony of FREEH’s statement that: “We are accountants. We can make numbers show whatever we want.” We also agreed with FREEH’s testimony that in this case, “[A] completely accurate reconstruction is not possible…we are all giving estimates. The question is…which is the best estimate?” In addition to the above, we found FREEH’s description of the auditing process to be blunt, understandable and enlightening.

Even though we were impressed by FREEH’s candor and her knowledge of auditing, we cannot adopt the “expectation analysis” that she proffered as an alternative to M&A’s more comprehensive analysis. FREEH testified that she developed her “expectation tolerance” depicted on Exhibit 8-A by combining three data sets:

(1) The average of the distributions during the four years preceding 2004-2007;

(2) The average of the distributions for the four years following 2004-2007;

(3) An analysis of the per capita wage derived from the 2000 census and Pennsylvania’s “weekly wage index.”

We do not agree with the first and third components of FREEH’s expectation analysis. The first component (average of four years preceding 2004) effectively reinforces the incorrect distribution scheme that the BUREAU was employing between 2004 and 2007. For the four years preceding 2003, the BUREAU was using the stale hard-wired computer percentages from 1992-1994, and it was using incorrect tax rates for four school districts and municipalities. We simply do not believe that a viable expectation analysis of a suspect class of data should be analyzed using data identical to that which was suspect. With respect to the third component employed by FREEH, we note that the census data was from the year 2000, and had not been updated to reflect any shifts in population that occurred thereafter. Even more important is the fact that the weekly wage index was derived from statewide statistics that calculated how individuals across the state of Pennsylvania were paid. As anyone who resides in this community knows, the differences between Lebanon and cities such as Philadelphia are as vast as the differences between the planets Mercury and Neptune. We reject any use of statewide wage information as a benchmark to determine how Lebanon County earned income should have been distributed.

We did not find FREEH’s expectation analysis set forth in Exhibit 8-A to be credible. We therefore reject it as a viable alternative to M&A’s more detailed analysis.

(8) BOWERCRAFT testified that he and three other M&A “team members” spent roughly 500 hours undertaking the analysis that had been discussed with the BUREAU and its constituencies. This is a significant investment of time and effort that we cannot and will not discount.

Perhaps more important than any other factor, we have been given information that would enable us to “test” the M&A analysis by comparing it with what everyone has agreed is accurate data created by KEYSTONE. Specifically, we have been given KEYSTONE’s actual distribution figures for the years 2009 through 2012. Because no one has questioned the accuracy of KEYSTONE’s data analytics, we view the KEYSTONE distributions between 2009 and 2012 to be the “gold standard” by which earned income tax should be distributed in Lebanon County. This conclusion is bolstered by the fact that BOWERCRAFT, SMITH, HOUSER and FREEH all relied upon the KEYSTONE data in one way or another, and DUFFUS wished that he would have had said data available to him when he completed his analysis.

The following chart is derived from information that no party has disputed. Column one represents the aggregate distribution to all five DEFENDANTS by KEYSTONE between 2009 and 2012. Column two represents the proposed distribution by M&A for years 2004 through 2007. Column three represents the actual distribution by the BUREAU – which the DEFENDANTS seek to have us adopt – between 2004 and 2007:

Municipality KEYSTONE M&A BUREAU

|

Bethel |

$1,810,497.00 |

$1,675,263.00 |

$1,745,834.00 |

|

Cornwall |

$2,043,578.00 |

$1,864,735.00 |

$2,921,413.00 |

|

Heidelberg |

$1,388,548.00 |

$1,410,718.00 |

$2,177,549.00 |

|

North Annville |

$ 969,768.00 |

$ 857,017.00 |

$1,132,431.00 |

|

West Cornwall |

$ 827,131.00 |

$ 798,039.00 |

$ 927,627.00 |

TOTAL:

$ 7,039,522.001

$ 6,605,772.002

$ 8,904,854.003

Simple math reveals that there is a difference of $433,748.00 between M&A’s calculations and the KEYSTONE “gold standard.” On the other hand, the BUREAU’s actual distributions to the five DEFENDANTS were $1,865,334.00 greater than the amounts distributed by KEYSTONE. To put this in perspective, the aggregate variance between KEYSTONE’s distribution to the DEFENDANTS and M&A’s calculation of what should have been distributed is 6%. In stark contrast, the variance between KEYSTONE’s distributions and the actual amount distributed by the BUREAU to the five DEFENDANTS is 26%, or over four times greater than the variance that relates to M&A’s calculations. We place significant weight on the fact that KEYSTONE’s accurate distributions between 2009 and 2012 so closely aligns with the distribution proposed by M&A, while it bears little comparison to the actual distributions undertaken by the BUREAU.

Could M&A have done better? Yes, it could have. We were disappointed by the relatively small test sample size of 120 local tax returns used to verify taxpayer residence. In addition, at least some of the existing local tax returns could have been matched with Department of Revenue data to test the difference in income between the Department of Revenue data set and local tax returns. In addition, we would have preferred to receive additional hard data to measure the degree to which S corporation income created a difference between state and local revenue calculations. Still, these imperfections of M&A’s analysis will not cause us to reject its findings.

Under Pennsylvania law, a plaintiff must prove damages “with a fair degree of probability.” Wujcik v. Yorktowne Dental Assoc., Inc., 701 A.2d 581, 584 (Pa.Super. 1997). However, “recovery will not be precluded simply because there is some uncertainty as to the precise amount of damages incurred. It is well established that mere uncertainty as to the amount of damages will not bar recovery where it is clear that damages were the certain result of the defendant’s conduct.” Pugh v. Holmes, 405 A.2d 897, 909-10 (Pa. 1979). Stated differently, “[W]hile damages cannot be based on mere guess or speculation, yet where the amount may be fairly estimated from the evidence, a recovery will be sustained even though such amount cannot be determined within entire accuracy.” Osterling v. Frick, 131 A. 250, 251 (Pa. 1925).

While we recognize that M&A’s analysis was imperfect, we find it to be a fair and reasonable reconstruction of how the BUREAU should have distributed tax revenue between 2004 and 2007. We also conclude that M&A’s distribution percentages are infinitely closer to what SMITH described as “the ideal world” than were the actual distributions by the BUREAU that the DEFENDANTS ask us to endorse. To summarize, we find as a fact that the percentages of distribution determined by M&A are fair, reasonable and based upon sound methodology, painstaking research and unassailable mathematical calculations. We therefore adopt Tables 3, 4, 5 and 6 from M&A’s report (Exh. 3) as our own findings of fact.

B. General Principles of Equity

Almost since the inception of the Republic, the law has recognized that mistakenly received monies must be repaid. Using a variety of equitable theories, Courts have consistently declared that when funds are mistakenly or wrongfully received, the recipient has an equitable and moral duty to return the funds and property to their rightful owner.

In Union Trust Co. v. Gilpin, 84 A. 450 (Pa. 1912), Pennsylvania’s highest court was confronted with a situation where monies were paid to the Defendant as a result of what the Court characterized as “a blunder,” Pennsylvania’s Supreme Court cited a general rule of law articulated by the Connecticut Supreme Court and stated:

We mean distinctly to assert that where money is paid by one under a mistake of his rights and his duty, and he was under no legal or moral obligation to pay, and which the recipient has no right in good conscience to retain, it may be recovered back in an action of indebitatus assumpsit whether such mistake be one of fact or law; and this we insist may be done both upon principal of Christian morals and the common law.

Id. at 450. This principle has been affirmed many times as part of Pennsylvania’s common law. In First Nat’l Bank of Monongahela City v. Carroll Twnshp., 27 A.2d 527 (Pa.Super. 1942), the Superior Court stated:

We have a long line of decisions which hold, in effect: ‘where one has in his hands money which in equity and good conscience belongs and ought to be paid to another, an action for money had and received will lie for the recovery thereof. No privity of contract is necessary to sustain this action, for the law, under the circumstances, implies a promise to pay.

Id. at 530, citing McAvoy and McMichael, Ltd. v. Commonwealth Title Ins. & Trust Co., 27 Pa.Super. 271, 1905 WL3585 (Pa.Super. 1904); Cameron Bank v. Aleppo Twnshp, 13 A.2d 40 (Pa. 1940); Greenwich Bank v. Commercial Banking Corp., 85 Pa.Super. 159, 1925 WL 4943 (Pa.Super. 1924).

At multiple times during the course of this litigation, the parties have cited the case of Brubaker v. Berks Co., 112 A.2d 620 (Pa. 1955). In Brubaker, the Court dealt with a situation similar to the one at bar. In Brubaker, the Plaintiff gave two checks totaling $7,000.00 to Samuel N. Moyer for the purpose of purchasing real estate. At the time, Mr. Moyer served as County Treasurer of Berks County. Either intentionally or by mistake, Mr. Moyer deposited the $7,000.00 checks into the County treasury. After Moyer died without completing the proposed real estate transaction, Brubaker sued the County to recover the amounts Moyer had wrongfully deposited into the County treasury. The Court analyzed the above facts through the lens of equity and stated:

Looking at this entire transaction through the eyes of abstract justice, one can come to no conclusion other than that Brubaker is entitled to his $7,000. Moyer had no right to turn the money over to the County and the County had no ethical or moral right to keep it once it was ascertained that the money in no way belonged to the County. Coming to this conclusion of natural justice, it would be shockingly incongruous if the law were to stamp on the money a title of County ownership simply because, through some adroit maneuvering on the part of the Treasurer, the money had fallen into the County’s coffers…

It is to be remembered, however, that the $7,000 was not taken from the County Treasurer but from the plaintiff Brubaker who certainly owed the County nothing. If the plaintiff had accidentally left his wallet on the County Treasurer’s desk and the Treasurer had dropped it into the County till, it could not be maintained with any semblance of law and justice that the County became the legal possessor of it.

Id. at 622-623.

As in Brubaker, the improper acts of an additional defendant – Moyer in Brubaker and BUREAU in this case – created an overpayment that was retained by the Defendants. Also as in Brubaker, the Plaintiffs suffered financial loss as a result of the Defendants’ retention of funds. In Brubaker, the Court imposed responsibility for the return of the monies upon the entity that retained them. So too will we.

From the above, we conclude from long-standing Pennsylvania precedent that when monies are mistakenly paid, the recipient has a moral and ethical duty to return the funds to their rightful owner. In addressing the specific causes of action proffered by PLAINTIFFS we will apply this general precept of equity of law and equity.

C. Unjust Enrichment

Unjust enrichment is a doctrine founded on principles of equity. “The polestar of the unjust enrichment is whether the Defendant has been unjustly enriched; the intent of the parties is irrelevant.” Limbach, LLC v. City of Philadelphia, 905 A.2d 567, 577 (Pa.Cmwlth. 2006). The elements of unjust enrichment in Pennsylvania are:

(1) A benefit conferred on a defendant by a plaintiff;

(2) Acceptance of such benefit by the defendant; and

(3) Retention of the benefit under such circumstances that it would be inequitable for the defendant to retain it.

See, e.g. Schenck v. K.E. David, 668 A.2d 327 (Pa.Super. 1995); Styer v. Hugo, 619 A.2d 347 (Pa.Super. 1993); Braun v. Wal-Mart, 24 A.3d 875 (Pa.Super. 2011).

In Caskie v. Philadelphia Rapid Transit Co., 184 A.17 (Pa. 1936), Pennsylvania’s highest court declared that privity of contract is not necessary to establish a claim for unjust enrichment. The Court declared that the key question in any unjust enrichment case is whether the Defendant “received money or property which he is not entitled to keep and which in equity and good conscience should be paid to Plaintiff in accordance with principles of natural justice.” Id. at 19. This principle was reaffirmed more recently in the case of Hughley v. Robert Beech Assoc., 378 A.2d 425 (Pa.Super. 1977), where the Superior Court held:

Where one has in his hands money which in equity and good conscience belongs and ought to be paid to another…no privity of contract is necessary to sustain this action, for the law, under these circumstances, implies a promise to pay…it makes no difference that it is from someone other than the Plaintiff that the Defendant received the money.

Id. at 427, citing Caskie, supra at 19.

In our opinion, the PLAINTIFFS have proven all elements of unjust enrichment. PLAINTIFFS have established that monies were paid to the DEFENDANTS that exceeded what the DEFENDANTS were entitled to receive. This constituted a “benefit.” Even until this day, the DEFENDANTS have continued to retain those “benefits.” Moreover, we conclude that it would be “inequitable” to permit the DEFENDANTS to retain tax monies that should have been paid to the PLAINTIFFS.

We cannot ignore the source of the money that is now in dispute; the excess monies paid by the BUREAU to the DEFENDANTS represented tax dollars paid by PLAINTIFFS’ residents. While everyone complains about taxes, at some level all citizens recognize that taxes are necessary in order for the government to provide needed services such as community policing, fire coverage, road maintenance, etc. In this case, the taxpayers of PLAINTIFFS complied with their civic duty to pay amounts intending that said amounts be used for the benefit of their own community. To permit monies paid by PLAINTIFFS’ residents to be used to benefit DEFENDANTS’ residents would, in the opinion of this Court, violate all principles of “natural justice.”

Based upon our initial factual conclusion that DEFENDANTS were overpaid at the expense of PLAINTIFFS, and based upon the law outlined above, we will find in favor of PLAINTIFFS and against DEFENDANTS on PLAINTIFFS’ unjust enrichment claim. As damages, we will require that the DEFENDANTS reimburse PLAINTIFFS for the amount of their overpayments plus interest on those overpayments from January 1, 2008. An accounting of these damages will be set forth below.

D. Constructive Trust

The doctrine of constructive trusts is another equitable cause of action that is very closely related to unjust enrichment. See Kimball v. Barr Township, 378 A.2d 366 (Pa.Super. 1977). A constructive trust arises “where a person holding title to property is subject to an equitable duty to convey it to another on the ground that he would be unjustly enriched if he were permitted to retain it.” 5 A. Scott, Law of Trusts, § 462 (3rd Ed. 1967); see also Yohe v. Yohe, 353 A.2d 417 (Pa. 1976); Kimball, supra. In describing a constructive trust, Pennsylvania appellate courts have repeatedly cited with approval the language of former Justice Cardozzo of New York in Beatty v. Googenheim Exploration Co., 122 N.E. 378 (N.Y. 1919):